【Morningstar】中芯國際發展或受美國潛在禁令威脅;台灣代工廠或受惠

Morningstar 2020-09-28 10:57

請至文末下載 PDF 檔,閱讀完整報告內容。

SMIC"s Expansion Threatened by Potential U.S. Ban

Reliance on imported semiconductor equipment to persist.

Executive Summary

The U.S. Department of Defense, or DoD, is, according to the media, considering banning U.S. suppliers from shipping to China"s leading chip maker, Semiconductor Manufacturing International Corp, or SMIC, without special permits, based on claims that SMIC has ties with China"s People"s Liberation Army, or PLA. If such a ban materializes, we think it would significantly impact SMIC"s operations, as an overwhelming majority of its equipment is sourced from U.S. or allied companies. Although Chinese substitutes have emerged in parts of the supply chain, their specifications are typically two to three generations behind. In this report, we outline three main possible scenarios ranging from no material impact to a forced stasis. We believe a ban on SMIC is only part of a greater Sino-American technological war and more Chinese companies in the supply chain are at risk of being banned.

Key Takeaways

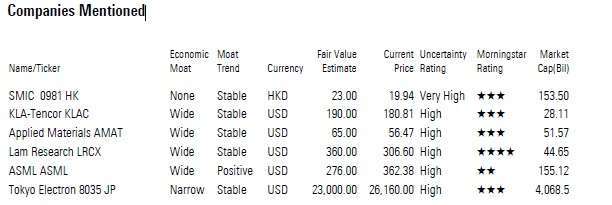

× While we maintain SMIC"s fair value estimate of HKD 23 per share pending confirmation from U.S. authorities, the mid- to long-term impact could be severe at a possible 40% downside risk, as there are no immediate Chinese deposition and inspection equipment substitutes. These areas are dominated by U.S. and Japanese players.

× In all our scenarios, China"s resolve in creating a self-sufficient semiconductor supply chain should point to more supportive policies. But this could also spur additional or prolonged U.S. complaints.

× We believe Taiwanese foundries United Microelectronics Corp., or UMC, and Vanguard International Semiconductor Corp., or VIS, could benefit from orders transferred from SMIC. Advanced Micro-Fabrication Equipment is a long-term beneficiary as its equipment is internationally competitive.

× If a ban does materialize, we expect China"s state-owned semiconductor companies like Datang Telecom, Yangtze Memory Technologies, or YMTC, JCET and GigaDevice to also be at risk, given their current business relationships with SMIC and/or Huawei.

Negative Impact to China"s Semiconductor Industry Is Inevitable

From Sept. 15, 2020, the U.S. mandates special permits for supplying semiconductors containing U.S. technology and intellectual property to Huawei, in principle. If strictly enforced, the rule prevents Huawei from sourcing even generic chips made by overseas firms. In fact, media reports indicate that Samsung Electronics and SK Hynix – which command more than 70% market share of the global DRAM market in total – are halting shipments of memory products to Huawei, while Samsung Display and LG Display have decided to suspend display panel shipments. The risk of not complying leaves these companies vulnerable to having their sales to U.S. companies curtailed.

Reuters reported that the U.S. government is also expected to require special permits for U.S. companies to transact with SMIC. As China"s largest semiconductor foundry, SMIC is obviously a key supplier to Huawei. If such a ban materializes, we believe the immediate impact may be manageable in the very short term, as SMIC can leverage its existing production facilities, and it is not reliant on U.S. raw material suppliers. However, it would clearly have a negative impact in the longer term, as SMIC’s ability to introduce more advanced nodes would be impaired.

We believe that such a ban would not only affect Huawei and SMIC, but also threatens Beijing’s intention to localize its semiconductor supply chain. The market share of semiconductor manufacturing equipment for Chinese suppliers is still small, and owing to the technological gap between China and the U.S., Japan and European suppliers, we believe it is difficult for SMIC to produce 40nm semiconductors from a fully localized production line, let alone the 5nm semiconductors that market leaders TSMC and Samsung Electronics have commercialized. This implies a 10-year gap in technical capability. YMTC, China"s first 3D NAND memory supplier, has similar plans to increase local sourcing of equipment and materials to 70%, from 30% currently.

As such, semiconductor equipment is one of the areas where the U.S. can exert heavy pressure. We think the Sino-American technological war will reinforce China’s intention to reduce its dependence on foreign suppliers. However, if a ban is introduced, we believe achieving such independence is even more challenging and there is likely to be negative impact on the Chinese semiconductor industry over the mid term.

Market concerns over a potential ban are more than enough to step up Beijing"s pursuit for a self-reliant supply chain, in our opinion. We think Beijing will continue to enact supportive policies for semiconductor players. In August 2020, the Chinese government revised tax exemption rules for domestic players that employ 28nm process or more advanced nodes. Possible policies may include providing more grants in semiconductor research in tertiary institutions, funding corporate research, subsidizing engineering academic programs, offering non-saleable land at nominal cost, waiving value-added tax for semiconductor equipment and materials, facilitating debt arrangements, and reforming state-owned entities by introducing private capital.

下一篇