Morningstar

請至文末下載 PDF 檔,閱讀完整報告內容。

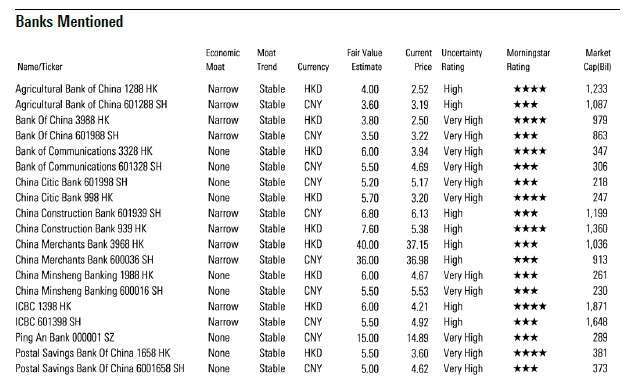

Reaffirming Our Confidence on Select Large Chinese Banks

Although the first significant net profit decline in over the past two decades for Chinese banks"first-half results was disappointing, we believe the market has already heavily discounted their valuations on concerns the pandemic, policy responses and a relaxation of credit policies will lead to increased risk to China"s banking sector. Because we see a more contained and more targeted monetary expansion push to support the economic slowdown, and as government rhetoric is less focused on hard growth targets, we expect lesser pressure for the banks to aggressively lend to support growth. This should lead to better risk management. As a result, we believe the headwinds are more than factored into the current valuations especially for our preferred banks China Construction Bank, or CCB, and Industrial and Commercial Bank of China, or ICBC. We also like China Merchants Bank, or CMB and its overall portfolio quality but its current share price indicates that it is fairly valued given risk rewards.

We think these three banks are better positioned to steer through the credit cycle challenges due to well capitalized balance sheets, strong risk buffers and cleaner loan book. A cleaner loan book is supported by the optimization of these banks"loan books over the past seven years and curtailment of shadow banking risks. During that period, the banks managed to strengthen their capital base, improve risk management and adopt stricter bad debt recognition. Though, we see increasing risks for large banks to reduce dividend payout if credit quality further deteriorates, our examination on future organic growth in banks" equity shows that equity financing risks for select banks should be well manageable given their strong capital position and return on equity.

Looking into the next two to four quarters, we believe potential upside catalysts include continued economic recovery, the progressive exit of the government"s pandemic measures, improvement in credit quality and provision level of banks and easing pressure on large banks" future capital needs.

Our positive long-term view for the select banks is also supported by a better interest rate environment, attributable thanks to the People"s Bank of China"s, or PBOC"s, targeted policy easing. We believe that the PBOC"s loosening policies will remain contained. As a result, we don"t expect the lending restrictions to the real estate sector to be relaxed. In addition, we also see the removal of hard GDP growth targets as reducing pressure on provincial governments to chase growth. Ultimately, this should allow the banking system to clear excesses and reduce risk.

上一篇

下一篇